By Justin Giovannelli, JoAnn Volk, Kevin Lucia, Ashley Williams and Kayla Connor

By Justin Giovannelli, JoAnn Volk, Kevin Lucia, Ashley Williams and Kayla Connor

Twitter: @commonwealthfnd

The promise of the Affordable Care Act (ACA) was not just to broaden access to health insurance, but also to enable more Americans to have coverage they could count on if they became sick. The health law sought to ensure that coverage would meet the needs of consumers by requiring that insurance for individuals and small businesses include 10 categories of “essential health benefits.” In 2012, states helped determine the package of essential benefits that health plans in their state were required to offer starting in 2014. Though states recently had the chance to revisit this decision for 2017 and beyond, most stayed the course and will continue to define essential health benefits much as they had before.

The back story. While the ACA identifies broad categories of medical benefits that plans must cover, federal regulations give states control over the specific items and services that comprise each benefit group. States exercise this authority, in part, by choosing an existing health plan to serve as a benefit benchmark. This procedure, along with other related policy decisions, allows states flexibility over benefit design. At the same time, this discretion has led to variation among states in what constitutes an “essential” benefit, with approaches differing with respect to coverage for autism, infertility, and pediatric services, among others.

Federal officials initially described the benchmark approach as “transitional” and promised to reassess it in time. They revisited it this year and decided to maintain the process through at least 2017.

The process of picking a benchmark. In 2012, and again this year, states were asked to choose a benefit benchmark from among 10 options (Exhibit 1). States that didn’t pick a plan were assigned a default choice: the largest health plan offered in the largest small-group product in the state. In 2012, about half of states selected a benchmark, while the remainder defaulted. The more active states (those that selected a plan) included almost all (15 of 17) of the states that established their own health insurance marketplace. This association has held: in 2015, 15 states that run their own marketplace again chose a benchmark, while two—the same states that defaulted in 2012, Idaho and Minnesota—did not.

Exhibit 1. Essential Health Benefit Benchmark Plan Selection Options

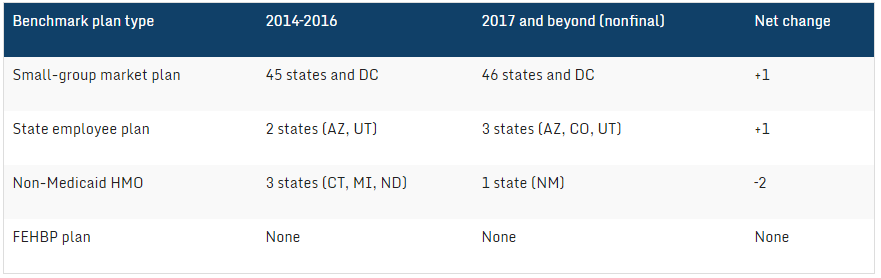

Meet the new benchmark, same as the old benchmark. By choice or by default, the vast majority of states ended up with a small-group plan as their benchmark in 2012. The list of states’ proposed benchmark plans for 2017 reveals little change (Exhibit 2).

Exhibit 2. State Benchmark Plans, by Plan Type and Benefit Year

Not only did states wind up with the same benchmark plan type; they also settled, overwhelmingly, on plans sold by the same insurance company. Only six states—Colorado, Georgia, Kentucky, New Mexico, North Dakota, and Pennsylvania—will peg 2017 benefits to a plan offered by a different carrier.

Looking forward. Federal regulators adopted the benchmark plan framework because they believed it promoted the ACA’s requirement of comprehensive coverage while helping states maintain flexibility. They retained that approach this year for the same reasons, but acknowledged they had little data from insurers—drawn from just one year (2014) of coverage—to consult to learn whether the policy was working.

That’s a vital point. To understand whether enrollees are having a hard time accessing needed care and determine whether the essential health benefits package needs to be modified—required tasks under the ACA—federal regulators need to harness more information on how consumers are experiencing their coverage. For example, claims data, including information on denials, could reveal service usage patterns that show how frequently consumers are accessing benefits not currently deemed essential by their state. Without these data, and others, it’s difficult to know whether consumers are well served by the benchmark approach or to evaluate the effect of federal policy changes regarding specific benefit categories, including habilitative services and prescription drugs.

Federal officials recently signaled they will begin to collect data from insurers under the ACA’s sunshine rules, provisions long in force but long unused. Unfortunately, the initial data call is quite limited, both in terms of the plans that must comply (a fraction of those subject to the transparency rules) and the information they must provide (generally, only company policies already publicly available). Regulators want and need a more complete sense of how the essential health benefits policy is working. They should use the disclosure tools available to them to find out.

This article was originally published on The Commonwealth Fund Blog and is republished here with permission.